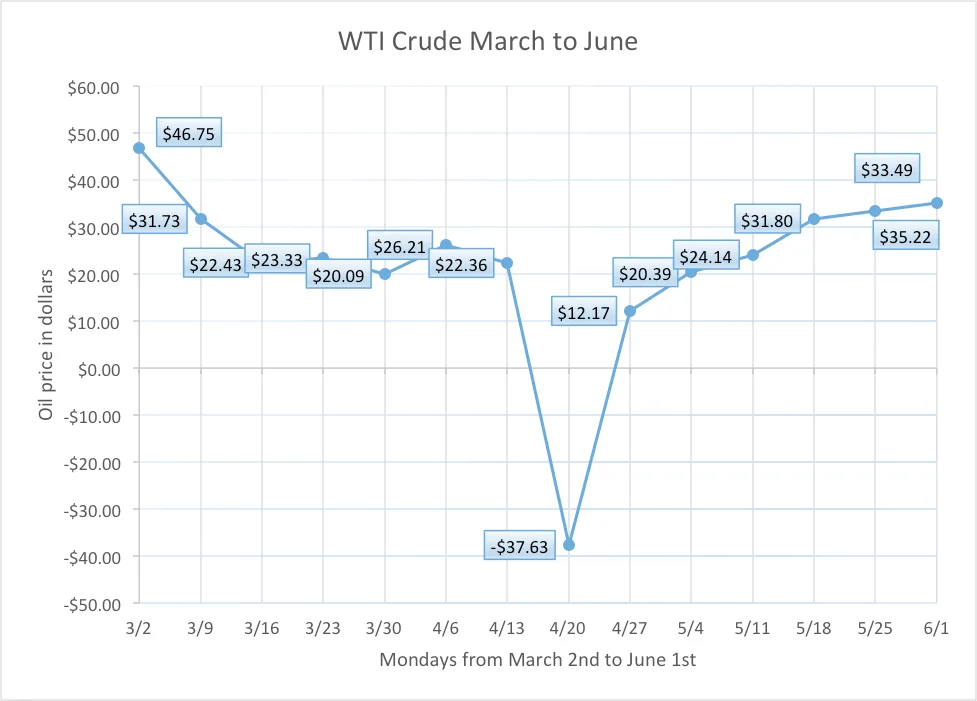

At the beginning of March 2020, the oil price war set a production crisis in motion for the oil and gas industry. The oil war between Russia and Saudia Arabia resulted in an unprecedented increase in the production of oil. The disagreement caused the West Texas Intermediate (WTI) price to drop from about $45 to $30 per barrel of oil. Before the lockdown due to Coronavirus Disease 2019 (COVID-19) was announced, the industry was already dealing with the threat of a surplus in oil and limited space to store it. By the end of March, President Donald Trump finally declared COVID-19, a national emergency. States began lockdown, and oil prices plummeted further as the result of lower oil demand. The price per barrel of WTI crude oil in March went from $46 to $20 a barrel. The combination of more supply and less demand for oil has created a troublesome situation within the industry.

In mid-April, oil prices went negative for the first time in history. The oil industry is looking at multiple cases of bankruptcies, with more expected to follow. Small and medium-sized oil companies felt the pressure even before larger companies announced layoffs and budget cuts. As oil prices continued to remain low, they were forced to stop production as they reached storage capacity. Those who struggled since March have tried different strategies to get used to the new norm. It leads to the critical question: “What are small and medium operations doing to adapt?”

How are small and mid-size operators adapting?

First, these operators look at where they can cut down on well optimizations and expenses. They remove as much as they can without affecting well production. Oilfield expenditures like rig workovers account for a large portion of operational costs. Eliminating these costs can still provide operators with consistent revenue. However, reducing capital and operational expenses while keeping up revenue is not enough to accommodate the low oil prices. Small and medium operators should begin with stopping well optimizations and see where they can reduce their expenses while continuing production.

As production continues, the operators need to decide whether to sell their commodity at a very low market price or keep it until the oil prices bounce back. Most smaller and medium-sized producers are shutting in their wells once their storages reach full capacity. Shutting in a well stops production. The oil and gas industry uses shut-ins for various reasons, but it comes at a price and risks. Shut-ins are more than an “off” switch. Extended shut-ins are known to cause damage to the well and negatively affect its production. Shut-ins should be used for a short period, and when storage capacity is full.

Some producers that decided to keep their oil are investing in frac tank rentals. They are outsourcing storage as their oil capacities are reaching their limits. They hope to keep their commodity long enough to avoid selling too low. Renting frac tanks gives the operators temporary storage and allows them to continue producing oil. Keeping and not selling oil is effective, as long as the price of oil stays very low. They are hoping the cost of storage is recovered when oil prices improve again. Smaller and medium-sized producers want to hold on to the commodity and sell it at a profitable price.

Producers that want to or have to sell their commodity are opting into a strategy known as hedging, more specifically with put options to minimize loss. The put option contract is purchased at a premium charge in dollars per barrel. It allows them to sell their commodity at the contract price instead of the monthly energy market price. Operators usually buy these contracts in advance because of fluctuating oil prices. They want to avoid selling oil at prices that are too low for them to continue running their operations. A quick example of put options, if the producer has a contract for $40 per barrel for this month and the market price for WTI crude is $35 when they sell, then the producer can avoid a face-value loss of $5 per barrel for that month. Put options have expensive premiums, and their costs increase with the volatility of the commodity. Hedging with put options is a strategy that requires planning with in-depth analysis because it involves understanding the energy market and the volatility of oil prices.

Conclusion

Small and medium-sized operators have a more difficult time with oil prices than the larger operators. Reducing their expenditures is the first step. They must consider how they can continue business during these uncertain times. They are stopping their production, finding storage amid a surplus on the market, and hedging prices based on the volatile oil price. Like most businesses, the oil and gas industry continues to be affected by the lowering demand for the commodity due to COVID-19. For small and medium oil producers, adapting to this economic change requires patience and taking calculated risks.