CONTENTS OF NEWSLETTER 38

- 311.The Risks of Abstract Logic

- 312. Share of Production

- 313. Copenhagen Conference Proceedings

- 314. Country assessment – Kuwait

- 315. World Oil Depletion Confirmed by a recent Minister in the British Government.

- 316. Shell downgrades its Reserves

- 317. Letter from Tehran

- 318. A Hint from the European Union

- 319. Third International ASPO Workshop in Berlin

- 320. Tarsand obstacles

- 321. How big is the biggest?

- 322. The Ethic of Zero Growth

- 323. Desperation in Britain

- 324. New Book on the Iraq Invasion

- 325. Future of the Newsletter

311. The Risks of Abstract Logic

Jules was an intelligent young man with a pleasing personality. He had completed his higher education at Louvain University in Economics and Logic, which he combined with a fertile imagination. He had had little difficulty in passing the entrance examination to the Directorate of Research of the European Commission.

His first task had been to react to complaints from an animal rights organization about the cruel treatment of pigs on their way to market. He had no prior experience of this subject but armed himself with a pig-breeders handbook from another department in the Commission. He read about the hormonal growth additives given to the pigs to improve their economic performance, but inspiration came to him sitting after lunch in the little garden he had discovered around the corner from his office in the Boulevard Woluwe when a butterfly alighted on the flower bed at his feet.

On returning to the office, he started writing his report, complete with many graphs, tracking distance to weight versus growth rate and stay occupancy. His solution was the addition of a synthetic butterfly hormone whereby the pigs would grow wings and be able to fly to market. Apart from the humanitarian benefits, the scheme showed impressive economic returns. His supervisors were delighted with the report, enabling them to assure the pig industry that they could now answer the concerns of the animal rights campaigners, and look forward to increased market share from aero-euro pork. A check with air traffic control classified the program as being within the dirigible Directorate.

That happy outcome made him a natural candidate to cover the next difficult issue facing the Commission, namely security of oil supply. He went to work with enthusiasm to develop a comparable model solution, whereby rising prices would stimulate both discovery and improved recovery, which sounded eminently logical. By this means, he was able to lift the expected ultimate recovery from the consensus of 1.93 trillion barrels of 65 published estimates by oil companies and knowledgeable institutions up to the year 2000 to an impressive 4.5 trillion by 2030. In some uniquely favored areas, as much as 70% would be recovered, despite the diversity of individual reservoir rocks and oil types so far observed in all oil producing areas. The ample recovery was further supported by reference to a study by the US Geological Survey, giving a wide range of estimated under alternative subjective probability rankings, which sounded impressively scientific being the result of 50000 iterations of simulation.

He refined the study further by considering OPEC, having near limitless resources, and Non-OPEC where limits were countered by intensive exploration yielding a discovery. A slight shadow of concern did flit across the page about OPEC’s willingness to supply, but he overcame that by saying that it was outside the scope of the study. (It has now been published by the European Commission under the title: World Energy, Technology, and Climate Policy Outlook – acronym WETO).

He fully deserved his promotion. He had helped his supervisors push that problem into the future when the possibility of miracles of biblical proportions could not be denied. Meanwhile, Business, as usual, was assured, as the sun shone with new intensity above the Rue de la Loi.

312. Share of Production

Work has commenced on the update of the ASPO depletion model to incorporate an interpretation of the production and reserve data for 2003, as published by the Oil & Gas Journal. It is a long and iterative process to try to tease out the most reasonable estimates. A preliminary result shows the following shares of production coming from the ten largest producers in 2000, 2005, 2010 and 2020. (The table on page 1 will be updated when the work is complete)

It is noteworthy that Russia heads the list in 2005 and 2010, and that the United States slips from 3rd to 10th place by 2020. Norway and the United Kingdom fall off the list by 2005 as North Sea production declines. The top ten producers account for between 60 and 70 percent of world production. It is a preliminary version subject to revision as the study progresses and refers to Regular Oil only. It is doubted that Saudi Arabia, which is treated as swing producer of last recourse, can meet the model’s demands upon it to 2020. More revision is called for.

We hear a great deal about “Reserve Growth, ” but it appears to be matched by “Reserve Erosion.” If we believed the Oil & Gas Journal reserve number of 1213 Gb for 2002, this year’s should be the same less the 65.43 Gb produced plus the 7 Gb reported to have been discovered, namely 1154 Gb. Instead of which 1266 Gb is reported. So, somehow 112 Gb has been added out of thin air. If we look at the numbers in detail, we see that as many as 68 countries report unchanged estimates with the singularly implausible implication that discovery or “reserve growth” exactly matched production. The estimates for some countries have remained unchanged for many years. In reality, the constant number probably reflects a failure to update the estimates or to respond to the Oil & Gas Journal. So, in the absence of information to the contrary, it seems better to reduce the reserve reports by the production during the unchanged period, which we could term “Reserve Erosion.”

![]()

313. Copenhagen Conference Proceedings

An excellent summary of the depletion issue has been published by Klaus Illum. A streaming video copy of the conference is also available.

314. Country assessment – Kuwait

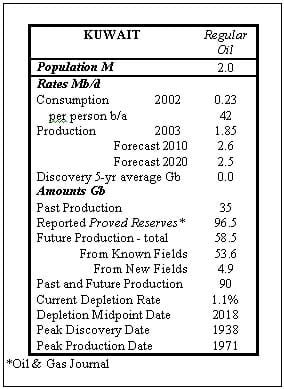

Kuwait is a small Emirate at the head of the Persian Gulf, covering an area of 18 000 km2 and supporting a population of about two million. Many are foreign workers from other Middle East countries and Asia. The average age is low with about 60% being under the age of 21. The majority are Sunni Muslims although one-quarter are Shi’ites, subject to a degree of mild oppression.

Also, Kuwait has an interest with Saudi Arabia in a 6000 km2 adjoining territory to the south, known as the Neutral Zone. It administers half the country directly and shares the total oil revenues with Saudi Arabia.

Kuwait lies at the mouth of the Euphrates and Tigris rivers and has long been a trading post serving the interior of Iraq. The Sabah family gained control in 1756 and has remained in power ever since. During the late 19th Century, Kuwait developed ties with the Ottoman Empire that controlled the surrounding territories but was never formally incorporated. Later, the country moved into a British sphere of influence, following the signature of a Treaty in 1899 by which Britain ran its foreign affairs. It became a British Protectorate following the First World War, losing a substantial amount of territory to Saudi Arabia in 1922, the Iraq boundary being settled a year later. Ownership of the deserts surrounding Kuwait City was largely immaterial until the discovery of oil, so it is not surprising that the boundaries are arbitrary and subject to certain disputes, resting perhaps on ancient tribal settings. Iraq first voiced such claims during the 1930s and may have lent some support to an abortive rising by Kuwaiti merchants against the Emir in 1938.

Britain imposed independence in 1961, as it withdrew from its empire after that Iraq strengthened its claims, not formally recognizing the country’s independence until 1963. The notions of nationality and territorial boundaries in the desert environment are probably foreign to the cultural tradition of the people, where family, tribal and religious allegiances are paramount. So the validity of Iraq’s claims may be stronger than might appear to western eyes.

The Iran-Iraq war of 1980 posed a certain threat to Kuwait. It found itself obliged to facilitate the entry of US and other armaments to Iraq, which the Iranians saw as a hostile act, leading to an attack on a Kuwait refinery and various subversive movements, one of which sponsored an attempted assassination of the Emir. No doubt the eternal Sunni – Shia conflicts were partly responsible. In 1986, Iran started to attack shipping in the Gulf, including particularly Kuwaiti tankers, which were then protected by the US Navy and placed under US flag.

In 1985, Kuwait arbitrarily increased its reported oil reserves by 50% although nothing particular had changed in the oilfields, in a successful effort to thwart its contractual OPEC production quota agreement, which was partly based on reserves. It also started pumping oil from the southern end of the Rumaila Oilfield, which straddles the border with Iraq (known as Ratqa in Kuwait). These actions naturally offended its neighbor Iraq, which both lost revenue and physical oil as a consequence. World oil prices fell during the 1980s adversely affecting both the Saudi royal family and the Texan constituents of Mr. Bush Sr. The United States accordingly moved to press its then ally, Saddam Hussein, to intervene in the councils of OPEC to strengthen adherence to the agreed quotas, especially by Kuwait, one of the principal offenders. Evidently, a border incident to stop production in the shared oilfield was contemplated, but Saddam Hussein overstepped his mandate and decided to take the entire country, which he successfully occupied on August 2nd, 1990.

This action was universally condemned, leading the United States and its NATO allies to rush troops to the region, supported by forces from other Middle East countries. Iraq resisted pressure to withdraw but was eventually forced to do so when the United States and its allies mounted a massive military attack in January 1991, liberating Kuwait and moving 200 km’s into Iraqi territory. A cease- fire was declared a month later, after the death of perhaps 100 000 Iraqis. It was an uneasy peace, leaving Iraq subject to a trade embargo, which caused great suffering to the populace. In 2003, the United States and Britain used Kuwait as a staging point for an invasion of Iraq on the questionable pretext that it had developed sophisticated threatening weapons, despite UN evidence to the contrary. Since no such weapons have been found, some analysts have searched for an alternative explanation for the invasion, seeing control of oil or support for Israel’s suppression of the Palestinians as possible motives.

The Emirate of Kuwait would indeed be of trivial world significance but for the substantial quantities of oil that lie beneath its sands. Its oil history is, therefore, more important than its political history. The featureless terrain of Kuwait did not at first seem very encouraging to the explorers who were familiar with the massive oil-bearing exposed anticlines of the Zagros Foothills of adjoining Iran. Interest in Kuwait’s potential was however stimulated by a New Zealand promoter, Major Frank Holmes. In 1927, he had interested Gulf Oil of Pittsburg in a concession to Bahrain, but this was opposed by the British Government, which controlled the foreign policy of the Gulf States. Britain later succumbed to US pressure, and in 1929 acquiesced to a proposal whereby California Standard (now Chevron-Texaco) would work Bahrain while BP (then the Anglo-Persian Oil Co) and Gulf would form the Kuwait Oil Company to work in Kuwait. BP was fairly skeptical of the prospects but wanted to keep control of what it saw as an American incursion into the Middle East, which was then a British sphere of influence.

Finally, in 1934, a 75-year concession for Kuwait was signed by the Emir. Finding a location for the first well in the featureless desert was no easy task, and the first well, completed in 1936, failed, prompting the companies to run a primitive seismic survey to map the subsurface. That was rewarded in February 1938 when the giant Burgan field was discovered at a depth of only 1120 m, with some 60 billion barrels of oil. Exploration resumed after the Second World War in Kuwait itself and commenced on the adjoining Neutral Zone where Jean-Paul Getty secured rights. He summed up his experiences with an immortal comment: “The meek may inherit the Earth but not its oil rights.”

In 1974, Kuwait effectively nationalized 60% of the Kuwait Oil Company, and took the remainder a year later, eventually paying compensation of $50 million to Gulf and BP.

There are several rich source rocks in the geological succession, but possibly the prime contributor in Kuwait are Middle Cretaceous claystone that develops on the flanks of the structures beneath a mild unconformity. Lower Cretaceous sandstones form the major reservoirs.

Two prospective structural trends have been identified. One runs through the Burgan Field northwards into Iraq, while the other forms an extension of the Safaniya trend of Saudi Arabia through the outer part of the Neutral Zone offshore. It appears that the intervening zone, covering the eastern Neutral Zone and Offshore Kuwait, is not particularly prospective. Likewise, the western platform has limited potential. There may, however, be scope for finding deep gas-condensate in an underlying Palaeozoic petroleum system

The main fields are as follows:

In total, some 85 Gb have been discovered in Kuwait with an additional 12 Gb in the Neutral Zone. Past production amounts to respectively about 36 and 7 Gb (including an estimated 6 Gb. which was lost when the wells were fired during the Iraqi retreat). Future discovery is here estimated at 5 Gb for Kuwait and 3.5 Gb for the Neutral Zone. Production peaked in 1971 at 2.9 Mb/d but then fell as a result of OPEC restraint. Both territories may be treated as members of the Swing Producers, making up the difference between world demand and what the other countries can produce, up to 2010. World demand is assumed to be flat to that date. Under such a scenario, (also making certain assumptions about the allocation of production within the Middle East swing producers), Kuwait’s production is expected to rise from a present 1.8 Mb/d to a second peak (depletion midpoint) at 2.7 Mb/d in 2018, before entering its terminal decline at about 2% a year. It may, however, prove to be unduly optimistic as reports speak of the rising water-table in Kuwait’s fields, now producing as much water as oil. So, some further reduction in the reserve estimates may be due.

Although still very much an Emirate under the long-standing Sabah family, the country does operate an elected National Assembly, albeit subject to periodic suspension if it shows signs of independence.

The Kuwait Oil Company moved downstream into Western Europe in the 1980s through its marketing chain Q-8 and has used its substantial oil revenues to fund massive western investments, probably largely for the benefit of the ruling families.

On the face of it, Kuwait is likely to remain firmly in the Western Camp, as a defense against claims and threats from its neighbors. It is also possible that the growing, young and largely disaffected population, many without local roots, may tire of a subsidized life in the coffee shops and react to Western interference in the Middle East. If a new Shia State should emerge from the ashes of southern Iraq that might galvanize the local Shia community into action, or stimulate a popular rising to overthrow the regime. Rising oil prices, which are virtually inevitable as shortages bite deeper, will make Kuwait an immensely wealthy place. At first, this may allow its substantially feudal government to buy off a disaffected population but on the other hand may prove to be a destabilizing influence. It is never easy to be a rich man in a crowd of beggars.

315. World Oil Depletion Confirmed by a recent Minister in the British Government

Michael Meacher, who was a Minister in Blair’s Cabinet from 1997 to 2003 has written a remarkably forthright article in the prestigious Financial Times entitled “Plan now for a world without oil” quoting ASPO. A highlighted paragraph summarizes its message:

“It is hard to envisage the effects of a radically reduced oil supply on a modern economy or society. Just such a radical reduction is staring us in the face.”

316. Shell downgrades its Reserves

Shell caused a furor in investment circles by downgrading its reported Reserves by 20%, namely 2.7 Gb for oil and 7.2 Tcf of gas, causing the shares to fall in value by about 10% in three days. The Company’s Chairman, Phil. Watts came in for much criticism. The amazing scale of payments to such luminaries was also revealed: the unfortunate Watts of Shell gets only $2.7 million a year, compared with Browne of BP at $8.4 and Raymond of ExxonMobil at $25.8 million. The beautiful palace and gardens at Versailles, built by Louis XIV in an earlier epoch of excessive privilege, survive for the enjoyment of later generations. Watts is described by the Wall Street Journal as a keen gardener, so there is hope yet.

Shell’s action drew attention to the SEC reporting rules, which are widely misunderstood. If properly reported, the term Proved Reserves in plain language means Proved-so-Far by current wells, and are about as secure as can be. But there is an additional category termed Proved Undeveloped (PUD), which means that the amounts in question are there to be produced but that the commercial decisions to produce them have not yet been made. It sounds an eminently sensible system for financial purposes. Shell’s reduction applied to the Proved Undeveloped category and is not in itself particularly significant as the timing of investments in remote and difficult countries such as Nigeria is obviously subject to unpredictable factors.

It is important to distinguish these strictly financial terms from those applied to the technical assessment of the volumes of recoverable oil in a prospect or oilfield. Proved Reserves in this sense means confirmed by producing wells; Probable Reserves mean likely additions from subsidiary corners of the field that have not yet been fully confirmed, and Possible Reserves refer to the possibility for example of a subsidiary deeper reservoir. These are sound pragmatic terms that can be easily understood by anyone. Modern practice, however, prefers to describe reserves regarding so-called Probability, distinguishing those with a high “chance,” better say than 90%, whatever that means given that each field is unique, from those with a low “chance.” This gives a range from which Mean, Mode, and Median values may be computed, in some cases with the intervention of so-called Monte Carlo Simulation whereby every combination of the various parameters is considered in as many as 50 000 iterations.

The technical estimation of reserves is not particularly difficult, whichever system is used, but like all accounts are subject to distortion and deliberate confusion for ulterior purposes. In fact, Shell deserves credit not condemnation for its frankness. The real message is that it has now exhausted its inventory of under-reported reserves that in the past could have easily compensated for these specific setbacks. A few years ago, the General Manager of BP was heard to comment that he did not think it was “quite cricket” to claim all the company’s reserves during his term of office, which he saw as unsporting treatment of his successor. Those days are evidently over as the industry faces the raw reality of depletion with the gap between consumption and discovery widening. Reserve Growth, so beloved by the USGS, is giving way to Reserve Erosion.

317. Letter from Tehran

Mr. Ali Samsam Bakhtiari, the well-known oil analyst with the National Iranian Oil Company, who has contributed several penetrating studies at ASPO workshops, is publishing a new newsletter on oil forecasting and the general depletion situation. He may be contacted at am_samsam@yahoo.com.

318. A Hint from the European Union

Dr. Emilio Martines of the Istituto Gas Ionizzati del CNR in Italy writes as follows.

“I would like to point your attention to a picture appearing in the Green Paper on Security of Energy Supply, published in 2000 by the European Commission (Page. 18). Despite the fact that in the text no explicit mention is made to the peak oil proximity, this figure (which I am attaching below) is in my opinion quite enlightening. Indeed, it shows clearly that beyond a daily production of the order of the present 75 Mb/day, the price of the additional barrel is expected to grow extremely fast. It is indeed a way of expressing the inability of the supply to cope with increasing demand. Unfortunately, no mention is made in the document to the source from which the picture came, nor the picture itself is commented in the text. It seems to be a sort of hidden hint.”

The meaning of cost is commonly clouded by uncertainty over what is included (exploration, amortization, tax, tax relief, bribes, military occupation, etc.) It could be argued that average cost will fall as an increasing share of world supply comes from the low-cost Middle East fields as the more expensive oil from other sources declines from natural depletion. Total production is set to fall both from natural depletion and soaring price as the producer’s profiteer from growing shortage. But it is interesting to find the European Union at least hinting that “business will not be as usual” much longer, whatever the precise meaning of the graph may be. (It has been redrawn for reproduction above).

319. Third International ASPO Workshop in Berlin

ASPO’s Third International Workshop on Oil and Gas Depletion will be held in Berlin on May 25th and 26th. It follows a successful meeting in Paris last year to which about 150 came from many countries. The program themes are as follows;

- Tuesday, May 25th

Morning: Natural Gas – Our Future?

Afternoon: Oil – When will production Peak? - Wednesday, May 26th

Morning: Renewables – What can we expect?

Afternoon: Energy and Society

A series of key presentations by invited speakers will be supplemented by poster sessions to capture ideas from a wider pool of researchers. There will be ample opportunity for formal and informal discussion, giving the participants a chance to meet each other in an attractive setting in Germany’s capital city. Full media coverage is anticipated. See www.peakoil.net for further details.

For planning purposes it would be helpful if those intending to attend could so inform the Secretariat as soon as possible: S.DeVries@bgr.de (tel. Sabine de Vreis +49 511 643 3208).

320. Tar sand obstacles

The following article confirms the difficulties to be faced in expanding tar sand production. It is noteworthy that the Energy Supply Board seeks to preserve value for Albertans. Such a concept appears to be in conflict with the provisions of NAFTA, whereby the United States is entitled to meet its mammoth energy needs by depleting Canada.

Alberta sets stage to decide on gas vs. oil fight

Friday, January 2, 6:13 pm By Jeffrey Jones

CALGARY, Alberta, Jan 2 (Reuters) – Alberta regulators released a key geological study on Friday that will serve as the basis for deciding how many natural gas wells companies will be forced to shut off to protect vast oil sands reserves.

The gas-versus-bitumen issue rocked energy markets last summer when the Alberta Energy and Utilities Board ordered 938 gas wells in the province’s northeast to be shut off as North American natural gas prices were surging, driving deep divisions between gas producers and oil sands developers.

Gas producers led by Paramount Energy Trust, anxious to keep supplies and their cash flow pumping, were allowed to apply for exemptions while the geological study progressed, however.

To the irritation of energy companies planning oil sands projects worth hundreds of millions of dollars, many of the wells remained to pump after the Sept. 1 deadline because of the exemptions.

The report, in which geologists from several major companies participated, did not detail which gas wells in the 22,000 square km (8,500 square miles), oil sands-rich Wabiskaw-McMurray region should be shut down for good.

Instead, board staff will use the data in the study to make recommendations on specific wells, which will be released on Jan. 26, it said.

Gas firms and producers of tar-like bitumen from oil sands, which is processed into refinery-ready crude, will be able to challenge the recommendations at a hearing set for March 8. At issue is that some of the gas in the region lies in contact with bitumen deep below the surface, and when the gas has produced the pressure in the bitumen reservoir drops.

The risk, say the board and oil sands firms, is that some of the crudes may not be able to be pumped to the surface using steam injection techniques, as is planned by several companies such as Petro-Canada and Nexen Inc.

They have argued that the gas pools are fast depleting and the energy content of the oil sands is 600 times higher. That value must be preserved for Albertans, the EUB has said.

“Over the next three weeks, we’ll be using the information, like the gas pools that are in contact and not in contact, and other information in the length and breadth of this document,” EUB spokesman Tom Neufeld said.

The study determined that 313 of 464 gas deposits in the region are not in contact with any oil sands reserves.

Currently, 330 gas wells are temporarily shut down, representing 40.5 percent of the area’s production.

Normally the region supplies about 2 percent of the gas output in Alberta, which is the biggest gas exporter to the United States.

Geologists who helped prepare the study work for such firms as Paramount, BP Plc, Petro-Canada, Nexen, ConocoPhillips and Devon Energy Corp.

(Reference furnished by Hans Jud)

321. How big is the biggest?

The World’s largest oil field is Ghawar in Saudi Arabia, but just how big is it? In 1975, when it was still managed by Chevron, it was reported to have held 60 Gb initially, of which 12.5 Gb had been produced, leaving reserves of 48 Gb. But this was no doubt a conservative estimate, being Proved Reserves possibly related to the then producing wells. The primary reservoir is reported to be about 220 ft thick, covering an area of about 700 000 acres (in good old oilfield units), which with another old rule of thumb of 400 barrels per acre-foot for a very good reservoir works out also around 60 Gb. By 2003, the field is reported to have already produced a total of about 53 Gb, implying by the old estimate that there are 7 Gb left. While the early Proved estimate was almost certainly very conservative, it is difficult to accept current reports that as much as 62 Gb remain. Taking a deep breath, one might suppose that the old 60 Gb number was about 30% under-reported, as was normal for most large fields, in which case the real number might be a rounded 80 Gb, meaning that about 27 Gb remain. The field is currently said to be producing almost 2.5 Gb/a and may have already peaked, is slightly down on the last few years.

It sounds like the field is about 70% depleted. If so, production is set to decline fairly steeply, especially when the water table rises to reach the horizontal wells that have been drilled to offset the natural decline. Perhaps a 10% annual decline would not be an unreasonable assumption. It is not unexpected, considering that it is not only the largest but one of the oldest fields. It had been identified before the Second World War, although development was delayed until 1948.

If this analysis is anywhere near correct for the largest field, we might suppose that the country’s reported reserves as a whole are also inflated by like amount, in which case the reported 260 Gb reduces to about 180 Gb. With an annual production of 2.7 Gb, this gives a depletion rate of about 1.5%, which is low by world standards, compared with about 7% in the North Sea for example, which further undermines the credibility of the reported higher number. Discovery too is falling with only about 6 Gb having been found in since 1990 to the extent that any reports can be believed. In short, we may conclude that the Middle East is subject to normal depletion and does not accordingly offer a limitless supply for the taking by military means or otherwise.

(Based partly on insight and information from J.Lyles)

322. The Ethic of Zero Growth

A splendid pamphlet by Ken Meyercord with the above title expresses compelling arguments and a form of a manifesto. It is obtainable from Zero Growth. Box 23924, Pleasant Hill, CA 94523, the USA at $3.00 and is well worth having. Oil depletion will surely deliver sub-zero growth, but this work presents the philosophical, environmental and humanistic reasons for welcoming rather than fearing the new World that opens as a consequence.

323. Desperation in Britain

As is becoming well known, the major companies are withdrawing from exploration in the North Sea, simply because they know that there is precious little left to find. They are also disposing of their less attractive interests and heavily depleted fields to smaller companies, presumably to put off the abandonment costs. In the face of falling exploration, government officials have been trawling the back streets of Houston and Calgary to encourage someone to come in and drill exploration wells on ever smaller and more dubious prospects. A new incentive has been reported of allowing the company is doing so a 150% tax write-off. This would be in addition to the write-off already available in the home country, which normally accepts exploration as a charge against taxable income. The speculator himself, therefore, bears barely any risk with the unconscious taxpayer footing most of the cost of the dry hole but should do well if the exploration should yield a freak discovery, as sometimes happens. He even probably does well while the activity in progress, whatever the outcome, as the venture attracts speculative interest in his company causing the share price to rise.

The taxpayer, if he were even remotely conscious of where his money was going, might wonder if there were not better ways of spending it. Perhaps Lenin got it right after all.

The London Times carried an important article on January 26th on the decline of the North Sea, referring to a study by Wood Mackenzie. It points out that the major companies are failing to replace reserves by discovery, and face the sensitive decision of when to stop exploration not paying its way. Britain has already become a net importer, as North Sea production declines steeply; and its experience is being repeated in one country after another. Wood Mackenzie stresses the scale of the problem by saying that the World needs to find the equivalent of a new North Sea every 18 months just to support current production, never mind meet any growth in demand.

As Schopenhauer said: “Truth passes through three stages: first it is ridiculed; second it is opposed, and third it is accepted as self-evident.” The issue of Oil Depletion has now reached the final stage

324. New Book on the Iraq Invasion

A penetrating new analysis of the background to the US wars and Iraq has been published jointly by the prestigious Bertelsmann Foundation, the Sais Bologna Center and the Robert Schuman Centre for Advanced Studies.

It is available online, being posted in the websites of the Bertelsmann Foundation (www.bertelsmann-stiftung.de), the JHU Bologna Center (www.jhubc.it) and the Robert Schuman Centre (www.iue.it/RSCAS/e-texts/Regime_Change_Iraq.pdf), from whence it can be freely downloaded. A hard copy version is forthcoming and can be ordered from www.iue.it/RSCAS/publications.

The chapter Pax Americana in the Middle East: Promises and Pitfalls by Professor Hudson are particularly revealing, as it identifies the elements within the US administration which were responsible, as well as the agendas that motivated them. It prompts but does not answer the sensitive question of who exactly was responsible for 9/11, the event that made possible the implementation of what was evidently a long-planned strategy.

325. Future of the Newsletter

This is the 38th Issue of the ASPO Newsletter which has grown from a humble beginning to be read by thousands. The task of compiling it grows ever more demanding with the receipt of 10-30 e-mails a day, many containing useful comments and material, while surface mail brings books, papers, articles, and letters, all of which demand grateful answers. Also is the database to be guarded, updated, and properly archived.

The subject is attracting increasing media interest with journalists, broadcasters and television producers seeking interviews. It is getting to be more than can be readily achieved by a single-handed geriatric. In short, the services of a secretary are urgently needed, at least part-time. One solution might be to make a small charge for the Newsletter to fund operating costs or publish a paper edition to the same end. Another would be to interest a charitable trust or foundation to sponsor the work. The style of the Newsletter is somewhat idiosyncratic hoping to raise challenging and sometimes sensitive subjects without falling through the thin ice of propriety. So far, it has attracted no more than one or two outbursts of outrage. Any ideas that readers might have about the future direction and possibilities would be very welcome.

Compiled by C.J.Campbell, Staball Hill, Ballydehob, Co. Cork, Ireland